Presents at Morgan Stanley’s 13th Annual Laguna Conference")

By Scott Kennedy, Produced with Colorado Wealth Management Fund

Introduction

Franklin BSP Realty Trust’s (NYSE:FBRT) results this quarter were mostly as expected. Their earnings/EAD dropped more than expected. The company’s big purchase of NewPoint could help earnings recover, but it will take time. At recent prices, we view FBRT as a buy, but cautious investors may want to wait.

Commentary

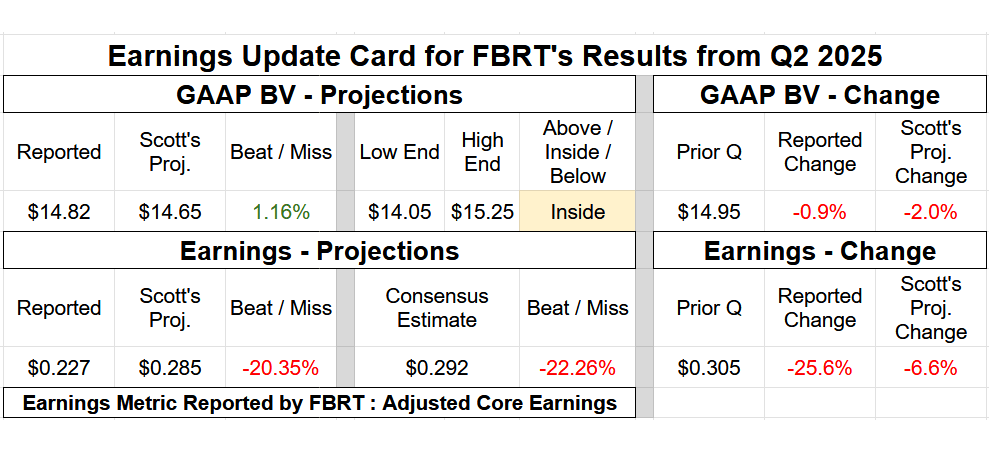

- Quarterly BV Fluctuation: Very Minor – Minor Outperformance (1.1% Variance).

- Adjusted Core Earnings/EAD: Modest – Notable Underperformance ($0.058 Variance).

A largely “as expected” quarter regarding Franklin BSP Realty Trust’s BV, in my opinion. If anything, a very minor—minor outperformance. FBRT recorded a very minor quarterly BV decrease, whereas I projected a minor decrease. Partially to a very minor net realized loss/write-off/REO transfer of 1 previously reserved-for property, FBRT recorded a quarterly net decrease to the company’s CECL reserves of $4 million (decreases are generally good). Part of this reserve decrease was also due to FBRT’s smaller investment portfolio size. Still, in my opinion, this was a bit “overly optimistic” due to the fact that FBRT added 3 new loans to the company’s “watch list” during Q2 2025. There was basically no accompanying new CECL reserves added for this event. In comparison, correctly assuming a particular medium-sized multifamily property would be transferred to REO assets and a couple more loans would be added to the watch list, I projected a quarterly net CECL reserves increase of ($15) million. As noted above, FBRT continued to actively take possession of an underlying troubled loan/property and transferred/converted it into an REO asset. REO assets are tested for impairment as opposed to specifically having CECL reserves (which pertain to loans). FBRT’s lower CECL reserves, when compared to my expectations, directly led to a BV outperformance of $0.21 per common share, which was the vast majority of the company’s overall quarterly BV outperformance of $0.17 per common share. The remainder of FBRT’s quarterly BV variance was basically the ($0.058) per common share underperformance within the company’s adjusted core earnings/EAD (discussed next).

FBRT’s modest-notable adjusted core earnings/EAD underperformance, which reverses applicable realized gains (losses) incurred during the quarter (similar sub-sector methodology), was mainly due to the following: 1) (6.5%) decrease in investment portfolio size when including REO sales (my projection was a mean decrease of only (2%)); 2) slightly lower investment portfolio effective coupon (7.85% during Q2 2025 versus my projection of 7.90%); and 3) slight underperformance in total operational expenses (mainly other expenses). Regarding origination volume, FBRT funded $321 million and only $91 million in loans during Q1 2025 and Q2 2025, respectively. Simply put, a modest-notable quarterly decrease that underperformed my mean projection of $225 million. In addition, FBRT had loan prepayments/repayments/amortizations of ($353) and ($317) million during Q1 2025 and Q2 2025, respectively. Simply put, still fairly elevated. In comparison, I projected quarterly loan prepayments/repayments/amortization of ($275) million during Q2 2025. In addition, FBRT sold ($84) million of the company’s accruing commercial MBS bonds during Q2 2025. This also directly resulted in lower net spread income/adjusted core earnings/EAD, which was disappointing.

So, FBRT’s minor quarterly BV decline largely matched expectations. However, FBRT’s notable quarterly adjusted core earnings/EAD decline was a negative surprise. While I correctly assumed “some” slowdown in operations in anticipation of the NewPoint Holdings JV LLC (NewPoint) acquisition (hence my projected minor quarterly adjusted core earnings/EAD decrease), the actual severity of this metric’s decline was disappointing.

While I continue to believe FBRT’s adjusted core earnings/EAD will increase as a direct result of the NewPoint acquisition, I also believe it is now a much harder “task” to increase the company’s adjusted core earnings/EAD from $0.227 per common share back to the current dividend level of $0.355 per common share. I know management believes they can move adjusted core earnings/EAD back to this level, but I believe that is if “all the stars align,” per se. However, that does not mean I believe a dividend cut is a 100% probability at this time. Management appears to be pretty confident that adjusted core earnings/EAD will move back to the dividend within the next year or so. Still, we have seen that “tune played before” regarding another fairly similar mREIT peer not too long ago, and we know how that played out (Ready Capital (RC)).

If it were not for the NewPoint acquisition, I probably would have downgraded FBRT’s recommendation ranges by (5%) or even (7.5%). However, I always try to remain non-biased in my assessments/judgements.

As such, along with my credit risk analysis below, I/we are performing a (2.5%) recommendation range downgrade to FBRT. However, this does not result in a risk/performance rating downgrade (remains at a 4.5). FBRT continues to have commercial real estate/multifamily loan exposure. Credit risk is something I am closely watching with FBRT. Potential credit risk had another “uptick” during Q2 2025 (2nd quarter in a row; discussed below). As such, I continue to anticipate new non-accrual loans at some point during 2025–2026 (at the very least, additional quick transfers to REO assets and/or write-offs on loan/property sales).

Change or Maintain

- BV/NAV Adjustment (BV/NAV Used Interchangeably): Our projection for current BV/NAV per share was adjusted: Up $0.15 (To Account for the Actual 6/30/2025 BV/NAV Vs. Prior Projection). Price targets have already been adjusted to reflect the change in BV/NAV. The update is included in the card below and the subscriber spreadsheets.

- Percentage Recommendation Range (Relative to CURRENT BV/NAV): (2.5%) Downgrade Results in a ($0.35) Per Share Recommendation Range/Price Target Decrease.

- Risk/Performance Rating: No Change. It remains at 4.5.

Earnings Results

The REIT forum

Note: BV at the end of the quarter. Subscriber spreadsheets and targets use current estimates, not trailing values.

Valuation

The REIT Forum

Ending Notes/Commentary

As a reminder, regarding setting an appropriate CECL, a very high degree of managerial judgment occurs/specialized expertise is needed. All of FBRT’s commercial whole loans are level 3 assets per ASC 820. Simply put, there is not a widespread, active marketplace for commercial whole loan pricing/valuations, as each mortgage (and underlying collateral) is unique. This makes setting valuations difficult, especially pertaining to impairment testing.

Regarding credit metrics, similar to the prior quarter, there was elevated activity that occurred during Q2 2025 regarding resolutions, transfers to REO, and/or new watch list loans. Simply looking at “top-line” metrics really does not tell the story. Upon performing a “deep dive” analysis, FBRT added 3 loans to the company’s “watch list” as of 6/30/2025 when compared to 3/31/2025. This was an AZ office, TX multifamily, and NC multifamily loan. I correctly projected that both multifamily loans would be added to FBRT’s watch list during Q2 2025. However, I was surprised the AZ office loan was (a bit cautionary/disappointing). However, within these 3 loans, 0 loans were placed on non-accrual status as of 6/30/2025, which is “cautiously optimistic” so far. In addition, as noted above, a previous watch list TX multifamily non-accrual loan was transferred to a REO asset and was partially written-off at the time of transfer.

Regarding FBRT’s acquisition of NewPoint, this officially closed on 7/1/2025. As such, the financial impacts of this acquisition will begin during Q3 2025. Management remains pleased regarding this commercial R/E finance company acquisition (which mainly specializes in multifamily operations). To reiterate, I believe this proposed acquisition is a net positive for FBRT (hence only the (2.5%) recommendation range downgrade on poor adjusted core earnings/EAD performance during Q2 2025 instead of a larger downgrade if this acquisition did not occur). NewPoint’s financials were just provided yesterday. As such, “final touches” to FBRT’s earnings modeling will occur in the near future (once earnings season winds down in a few weeks). I am not anticipating notable changes to my modeling, though (which already was incorporating NewPoint’s projected performance).

Even with a minor recommendation range downgrade, FBRT is currently deemed to be modestly undervalued. However, as echoed over the last 7 quarters, cautious subscribers may want to wait until more market participants believe it is safer to invest in commercial real estate as a whole (yes, even multifamily loans). I currently believe that, in a couple of years, FBRT’s stock price should be higher than its current per share amount. However, it will likely be a “bumpy/see-sawing” road over the next couple of quarters (as it recently has been).

Read the full article here

")